An AH-64 Apache helicopter launches an Altius 700 Medium-Range Launched Effect (MR-LE) during a recent exercise at U.S. Army Yuma Proving Ground. Army

Tiltrotor who? US military helicopter deliveries rose 13 percent in 2025

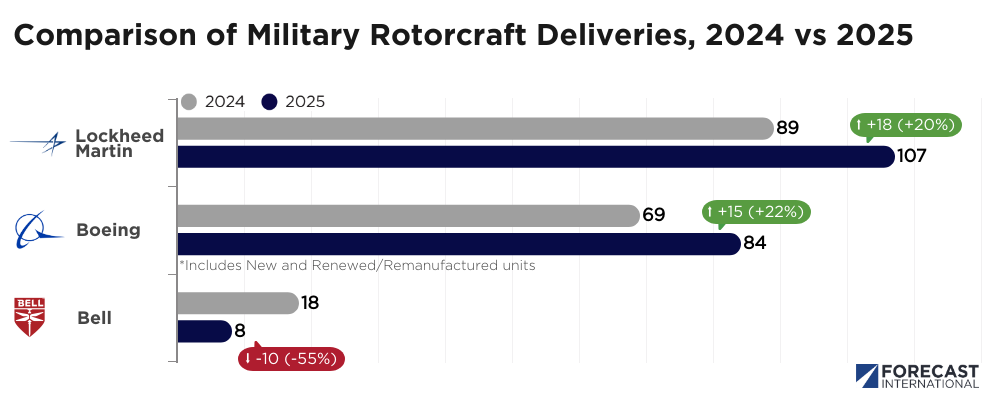

The Big 3 U.S. makers delivered more rotorcraft last year than in 2024.

With all the talk of tiltrotors, you'd be forgiven for believing the era of conventional rotorcraft is winding down. But last year, the big three American rotorcraft manufacturers—Bell, Boeing, and Lockheed Martin's Sikorsky—delivered a combined 199 military rotorcraft: 13 percent more than in 2024.

By the Numbers

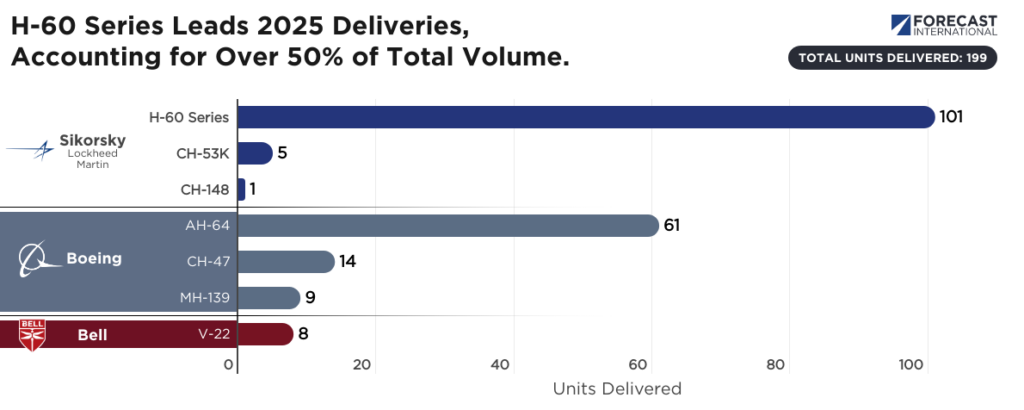

Sikorsky delivered the most in 2025, anchored by the H-60 line: a total of 101 Black Hawks and Seahawks. Boeing recorded the most growth, increasing annual deliveries by about 22 percent. Bell experienced the only decline among the three companies, delivering ten fewer aircraft in 2025 as AH-1Z exports taper and MV-22 Osprey production for the U.S. Navy and Marine Corps nears completion.

Fall 2025 showed huge contractual wins for Boeing and Sikorsky’s key military helicopter programs. Building on a long-developing agreement, Boeing announced in November that it will build 96 AH-64E Apache attack helicopters for Poland. The deal, valued at $4.7 billion, will make Poland the 19th operator of Apaches—and give it the largest fleet outside of the U.S.

Boeing also secured over $1.6 billion in contracts for its heavy-lift Chinook series late last year. Included in those awards are funding to accelerate U.S. Army fielding of the CH-47 Block II, agreements for the MH-47G for U.S. Special Operations Command, and $876.4 million to produce up to 60 CH-47F Block II helicopters for Germany.

Meanwhile, Sikorsky inked a historic $10.9 billion contract with the U.S. Navy, confirming the Marine Corps’ long-term commitment to the CH-53K. The five-year framework secures five production lots for up to 99 helicopters.

Defense One sister brand Forecast International projects Boeing to build more units from 2026 through 2030, but our estimates show that Sikorsky will build a larger share, about 40 percent, of the total market production value. This prediction is primarily due to the high unit cost of the powerful triple-engine King Stallion.

Tiltrotor Transition

Bell is producing fewer aircraft for the moment, as it prepares to introduce the MV-75 tiltrotor for the U.S. Army Future Long Range Assault Aircraft (FLRAA) program. Assembly work is now underway on the first test aircraft. Bell and the U.S. Army are prioritizing the rapid fielding of the MV-75, with initial production expected in the next one to two years.

Bell’s market position will rise during the mid-2030s as it approaches full-rate manufacturing of the MV-75. Cumulatively, the program could ultimately approach $70 billion. While Boeing and Sikorsky’s helicopter portfolios remain rooted in modernized legacy designs, the MV-75 represents the first clean-sheet U.S. rotorcraft since the joint Bell-Boeing V-22 Osprey entered service nearly 20 years ago.

As the military rotorcraft market moves from today's aircraft to tomorrow's in the next decade, the overall forecast remains robust. Bell, Boeing, and Sikorsky will produce nearly 600 units during the next three years. Meanwhile, rotorcraft demand remains strong in the broader market. European-based Airbus Helicopters delivered 31 more units in 2025 than the previous year across its civil and military product range. The company also reported 544 gross orders in 2025, up from 455 during 2024.

Hybrid Horizon

Naturally, the proliferation of uncrewed systems and drone warfare has raised questions about the viability of manned military rotorcraft. Nonetheless, current market signals project stability and reinforce the utility of these aircraft in contemporary environments. If anything, these forces are driving traditional prime contractors to integrate emerging technologies with their existing platforms while developing next-generation initiatives.

Hedging on the momentum of the U.S. Air Force Collaborative Combat Aircraft (CCA) program, Boeing debuted a similar drone wingman concept last October for accompanying U.S. Army rotorcraft. That same month, Sikorsky unveiled a tablet-controlled UH-60L helicopter, the U-Hawk, which features the company’s MATRIX autonomy suite. More recently, Sikorsky announced a joint project with the Robinson Helicopter Company–a world leader in civil rotorcraft–to integrate MATRIX with the R66 TURBINETRUCK, an autonomous helicopter built on the R66 airframe.

For its part, Bell has been working on uncrewed rotorcraft capabilities for years, most notably under a joint Defense Advanced Research Projects Agency (DARPA) and SOCOM program. Earlier this month, Bell announced that its Speed and Runway Independent Technologies (SPRINT) design entry received the designation X-76, clearing the way to build a high-speed demonstrator. That prototype will likely feature Bell’s revolutionary Stop/Fold rotor system to meet SPRINT requirements for a 400-plus knot aircraft that can operate from austere environments.

Proven Legacy

Uncrewed technologies aside, rotorcraft are demonstrating renewed mission versatility. Israeli and Emirati AH-64 Apache attack helicopters have reportedly downed Iranian Shahed drones in recent combat operations. Likewise, the U.S. Army is testing Apaches for Counter-UAS applications using the underslung 30mm cannon and guided munitions via Advanced Precision Kill Weapon System (APKWS) kits from the stub-wing pylons.

The integration of launched effects and standoff weapons, paired with doctrinal adaptation, is significantly enhancing rotorcraft survivability. High-speed tiltrotor design and uncrewed systems may define the future, yet conventional attack and utility helicopters remain vital, evidenced by market data and operational necessity.